Continuous Glucose Monitors and Insurance – Are You Covered?

Understanding Your CGM Insurance Coverage Options

CGM covered by insurance depends on your specific plan type, diabetes diagnosis, and treatment intensity. Here's what you need to know:

Quick Coverage Check:

- Medicare: Covers CGM if you have diabetes, use insulin, and meet 5 specific criteria

- Private Insurance: Usually covers CGM under durable medical equipment benefits with prior authorization

- Provincial Programs (Canada): Income-tested coverage available in most provinces for qualifying patients

- Employer Plans: Coverage varies but typically requires multiple daily insulin injections or pump therapy

Most insurance plans do cover continuous glucose monitors, but the approval process requires proper documentation from your healthcare provider. The key is understanding your plan's specific requirements and having the right paperwork ready.

What Makes You Eligible:

- Type 1 diabetes on any insulin regimen

- Type 2 diabetes with 3+ daily insulin injections

- History of severe low blood sugar episodes

- Pregnancy with diabetes requiring tight glucose control

The good news? CGM coverage has expanded significantly in recent years. Medicare removed many restrictions in 2023, and most private insurers now recognize CGMs as medically necessary rather than just convenient.

Coverage typically includes:

- The CGM receiver or smartphone app

- Sensors (usually 2-3 per month depending on device)

- Transmitters (replaced every 90 days to 6 months)

Simple cgm covered by insurance word guide:

How Continuous Glucose Monitoring Works & Why Insurers Care

Think of a continuous glucose monitor as your blood sugar's personal assistant - one that never takes a break. Instead of fingerstick tests that give you just a snapshot, CGMs track your interstitial glucose levels every few minutes, all day and night.

This tiny wearable sensor creates a complete movie of your glucose patterns, not just a single photograph. It sends alerts when your levels are heading too high or too low, often before you'd feel symptoms. For many people, it's like having a safety net that's always there.

Here's where it gets interesting for insurance companies: research shows CGMs aren't just convenient - they actually save money. People using continuous glucose monitors achieve better A1C levels and experience fewer dangerous low blood sugar episodes. When insurers see fewer emergency room visits and hospitalizations, they start paying attention to the bottom line.

The technology comes in two flavors that affect whether cgm covered by insurance applies. Therapeutic CGMs can completely replace daily fingerstick tests, while Professional CGMs are used for short-term monitoring - usually covered for up to six sessions per year.

Insurance companies follow clinical guidelines from respected organizations like the American Diabetes Association. These groups have recognized CGMs as essential tools for anyone on intensive insulin therapy, giving insurers the medical backing they need to approve claims.

Key Benefits That Drive Coverage Decisions

Insurance companies love numbers that prove value, and CGMs deliver exactly that data. The metric that gets the most attention is time-in-range - how much time you spend in your target glucose zone (usually between 70-180 mg/dL). More time in range means fewer complications and lower healthcare costs.

Fewer ER visits is another big win. When people can see their glucose trends in real-time, they catch problems before they become emergencies. This is especially valuable for people who can't feel when their blood sugar drops too low.

Remote monitoring capabilities have been game-changers, particularly for families with children who have diabetes. Parents can check their child's glucose levels from work, and adult children can monitor aging parents.

Data-sharing with healthcare teams means your doctor gets detailed reports about your glucose patterns between visits. This leads to better treatment adjustments and fewer "trial and error" medication changes.

Eligibility Based on Diabetes Type and Therapy Intensity

Your path to getting cgm covered by insurance depends on your diabetes type and treatment intensity. The rules are based on who benefits most from continuous monitoring.

Type 1 diabetes gets approval almost universally. Since people with Type 1 need insulin to survive, insurance companies recognize that continuous monitoring makes sense regardless of the specific insulin regimen.

Type 2 diabetes on intensive insulin requires at least three daily insulin injections or insulin pump use. This includes people managing complex regimens with both rapid-acting and long-acting insulin.

Gestational diabetes often qualifies during pregnancy when tight glucose control is critical. The stakes are high enough that insurers typically approve CGMs without much hassle.

Some plans also make exceptions for people who experience frequent severe hypoglycemia, even if they're not on intensive insulin therapy.

Is a CGM Covered by Insurance? Understanding Public, Private & Employer Plans

Here's the good news: cgm covered by insurance is now the norm rather than the exception. CGM coverage has expanded dramatically over the past few years, and most insurance plans do cover CGMs, though navigating the details can feel like solving a puzzle.

Medicare covers devices and supplies under their durable medical equipment benefit. Medicaid programs generally follow Medicare's lead, though each state adds its own requirements. In Canada, most provincial programs offer income-tested coverage through programs like BC PharmaCare and New Brunswick's insulin pump program.

Private employer plans typically cover CGMs either under medical benefits or pharmacy benefits. Individual marketplace plans are required to cover diabetes supplies, including CGMs for people who meet medical criteria. All CGM expenses are eligible for Health Savings Account reimbursement.

The CGM Insurance Look-Up Tool can save you time by letting you check your specific plan's coverage details.

"CGM Covered by Insurance" Criteria in Major Public Programs

Medicare's approach is straightforward once you understand their five-point checklist. You'll need a diabetes diagnosis, current insulin use, a prescription from your doctor, completed training on CGM use, and regular doctor visits. Medicare removed many restrictive requirements that used to make coverage difficult.

BC PharmaCare covers CGM sensors through their diabetes device program, using income-tested coverage based on your family's financial situation.

New Brunswick's program made fantastic changes recently. They removed the age cap in August 2023 and expanded coverage in October 2023. Now the program covers people with Type 1 diabetes at any age and Type 2 diabetes patients who need three or more daily insulin injections.

Each Canadian province has developed its own approach to CGM coverage. Some focus on age limits, others emphasize income thresholds, and most require specific medical necessity documentation.

"CGM Covered by Insurance" Rules in Private & Employer Policies

Private insurance plans usually categorize CGMs under their durable medical equipment benefit, though some plans treat them as pharmacy items. This affects where you get supplies and how much you pay.

Prior authorization is the gatekeeping step most private plans require. Your doctor makes a case to the insurance company about why you need a CGM. Once approved, renewals are typically much simpler.

Quantity limits are standardized across plans. For most CGM systems, you'll get enough sensors for continuous wear plus a small buffer. Transmitters are replaced every few months, and receivers are covered annually if needed.

Age restrictions vary by device, with some systems approved for children as young as 2 years old, while others require users to be 18 or older. Your insurance will follow the FDA-approved age ranges for each specific CGM system.

The medical necessity documentation your doctor submits needs to be recent - usually within the past 12 months. This includes prescription details, recent A1C results, and a clear statement about why continuous monitoring is medically necessary.

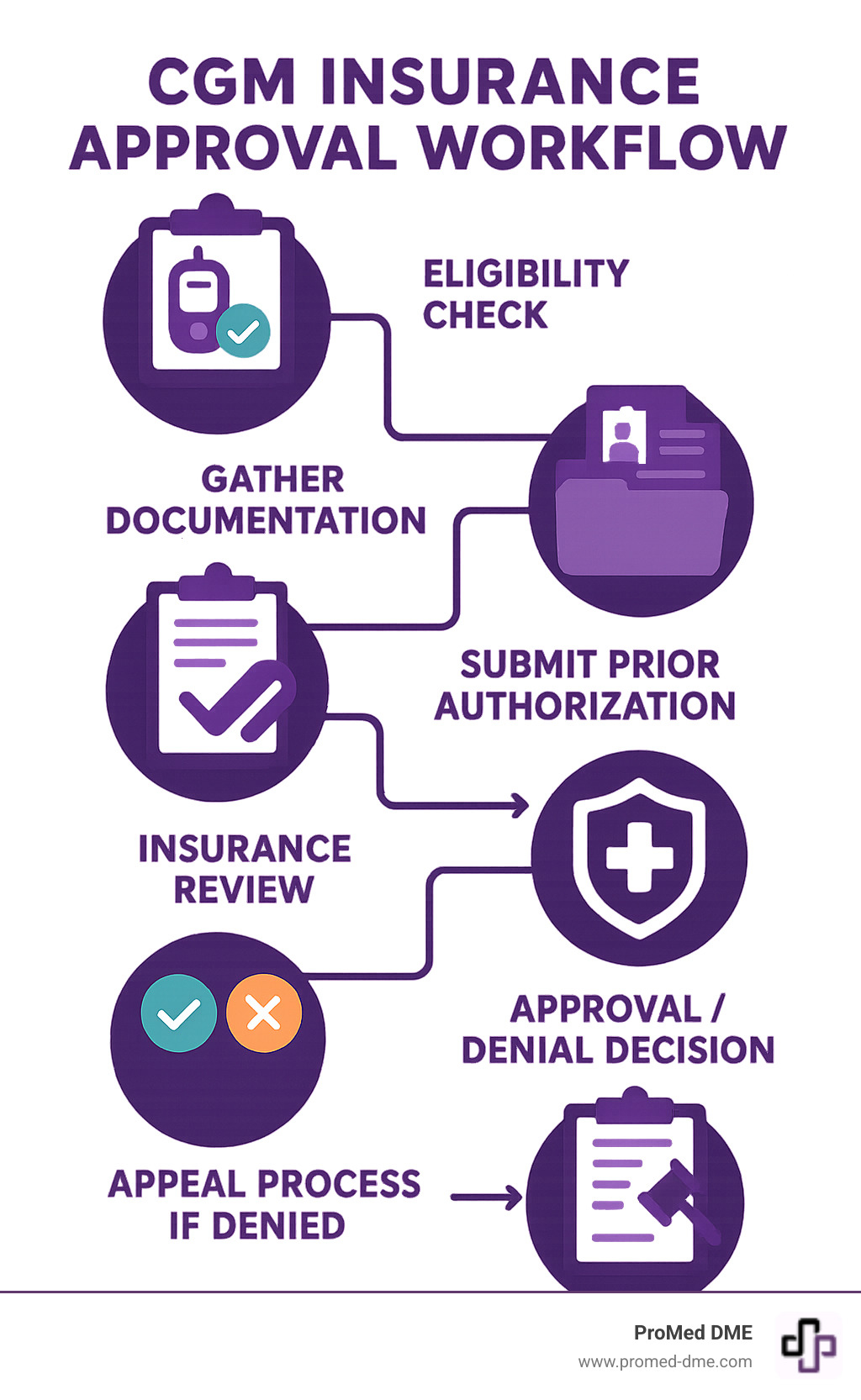

Getting Your CGM Approved: Step-by-Step Playbook

Getting your CGM covered by insurance doesn't have to feel overwhelming. While the process might seem complex at first, thousands of people successfully steer insurance approval every month. The key is knowing exactly what your insurance company wants to see and having everything ready before you start.

Think of this as building a case for why you need a CGM. Insurance companies need proof that the device is medically necessary for your specific situation. Once you understand their perspective, the approval process becomes much more straightforward.

Start by checking your coverage details through your insurance company's website or member services. You'll want to know if CGMs fall under your medical benefits or pharmacy benefits, since this affects where you'll submit paperwork. Most plans require prior authorization.

Your healthcare provider is your strongest ally in this process. They know the medical language insurance companies want to hear and can document your need for continuous monitoring. Schedule an appointment specifically to discuss CGM coverage.

The prescription needs to be detailed and specific. A simple "CGM device" won't cut it. Your doctor should specify the exact device model, sensors, transmitters, and any accessories you'll need. This prevents delays and follow-up questions.

Timing matters for renewal. Most CGM approvals last for one year, but start the renewal process about 30 days before your current approval expires to prevent coverage gaps.

Gathering the Paperwork Insurers Expect

Insurance companies want to see a clear medical picture that justifies CGM coverage. Your current A1C results show where your blood sugar management stands right now. Most insurers want results from within the past 12 months.

Your insulin regimen notes are the heart of your approval case. Insurance companies need to see that you're on intensive insulin therapy, which typically means three or more daily injections or pump therapy. Your doctor should document not just what insulin you take, but how often you inject it.

Documentation of hypoglycemia frequency can be a game-changer for approval, especially if you experience severe low blood sugar episodes or have trouble recognizing when your glucose is dropping. Even noting how often you check your blood sugar or wake up at night to test can show the need for continuous monitoring.

Training certificates show insurance companies that you're committed to using the CGM properly. Some plans specifically require proof that you or your caregiver has been trained on the device.

What to Do If Your Claim Is Denied

Getting a denial letter can feel discouraging, but initial denials are incredibly common, even for people who clearly qualify for CGM coverage. Insurance companies often deny first requests as a matter of course. Don't take it personally, and definitely don't give up.

A peer-to-peer review is often your fastest path to approval after a denial. This means your doctor gets on the phone with the insurance company's medical director to discuss your case directly. Doctor-to-doctor conversations can resolve misunderstandings quickly.

Filing a formal appeal gives you a second chance to present your case with additional documentation. Ask your healthcare provider to write a detailed letter explaining exactly why continuous glucose monitoring is medically necessary for your diabetes management.

Your state insurance commission can be a powerful ally if you're dealing with a private insurance company that seems to be inappropriately denying coverage. These offices investigate insurance practices and can often get results when direct appeals haven't worked.

External medical review boards provide an independent assessment of your case when internal appeals have been exhausted. Many states require insurance companies to offer this option.

Costs, Savings & Extra Help

Let's talk numbers - because knowing what you might pay for CGM supplies helps you plan ahead and find the best deals. The good news is that CGM covered by insurance typically reduces your monthly costs dramatically compared to paying full price.

Without insurance coverage, you're looking at hefty monthly expenses. Dexcom G6 and G7 systems run about $300-400 per month when you factor in sensors and transmitters. FreeStyle Libre sensors are more budget-friendly at around $150-200 monthly. Don't forget the initial receiver device, which is a one-time cost of $200-300.

With Medicare coverage, you'll pay 20% coinsurance after meeting your Part B deductible - often bringing monthly costs down to $60-80. Private insurance plans vary widely, but most people see monthly copays between $25-100 depending on their specific plan structure.

High-deductible health plans can mean higher upfront costs early in the year, but lower costs once you hit your deductible.

| Coverage Type | Typical Monthly Cost | Annual Out-of-Pocket |

|---|---|---|

| No Insurance | $300-400 | $3,600-4,800 |

| Medicare | $60-80 | $720-960 |

| Private Insurance | $25-100 | $300-1,200 |

| High-Deductible Plan | Varies by deductible | $1,000-3,000 |

Your actual costs depend on whether your plan covers CGMs under medical benefits or pharmacy benefits, your specific deductible and coinsurance structure, and whether you've already met your annual out-of-pocket maximum.

Co-Pay Assistance & Affordability Programs

Nobody should have to choose between managing their diabetes and paying rent. Thankfully, there are several programs designed to help make CGM supplies more affordable.

Manufacturer copay cards are often your best first step. Most CGM companies offer these programs, which can slash your monthly costs to as low as $25-50 per month, even if you have private insurance. These programs usually don't work with government insurance like Medicare or Medicaid.

Patient assistance programs step in when copay cards aren't available. These income-based programs can provide free or heavily discounted CGM supplies if you meet their financial requirements.

Health Savings Accounts (HSAs) are a smart way to pay for CGM expenses with pre-tax dollars. Since CGM supplies are HSA-eligible, you're essentially getting a discount equal to your tax rate.

Don't overlook tax deductions either. CGM expenses count as medical expenses, and if your total medical costs exceed 7.5% of your adjusted gross income, you can deduct the excess on your tax return.

Some states have created special diabetes device funds to help residents cover CGM supply costs. These programs typically have income requirements and may have waiting lists.

Nonprofit grants are another option, especially for families with children who need CGM devices.

Provincial & State Variations You Should Know

Coverage rules change dramatically depending on where you live, which can be frustrating if you're moving or comparing options across state lines.

Canadian provinces each handle CGM coverage differently. Some provinces recently removed age caps that previously limited coverage to children or young adults. Income thresholds vary significantly - what qualifies you for coverage in British Columbia might not qualify you in Ontario.

Device formularies also differ by province. Your province might cover one brand of CGM but not another, which could influence which device your doctor prescribes.

In the United States, Medicaid coverage follows each state's individual guidelines. Some states have generous diabetes coverage policies, while others stick to the bare minimum requirements.

State insurance commissioners take different approaches to coverage disputes too. Some states are more aggressive about requiring insurance companies to cover CGM devices, while others take a more hands-off approach.

The bottom line? Don't assume that coverage rules you hear about from friends or online forums apply to your specific situation. Coverage can vary dramatically even within the same insurance company based on your location and specific plan details.

Frequently Asked Questions about CGM Coverage

Let's tackle the three questions we hear most often about CGM covered by insurance - these are the ones that keep people up at night wondering about their coverage.

How long does CGM approval last and how do I renew?

Here's the good news: most insurance approvals last a full 12 months, giving you a whole year of coverage once you're approved. Some generous plans even approve coverage for longer periods, but annual renewal is the standard.

The renewal process is usually much simpler than your initial approval. Your healthcare provider will need to submit updated paperwork showing that you're still benefiting from CGM therapy. This typically includes fresh A1C results, confirmation that you're still on qualifying insulin therapy, and documentation that you're actually using the CGM as prescribed.

Think of renewal as a wellness check - your insurance company wants to see that the CGM is helping you manage your diabetes effectively. If your A1C has improved or stayed stable, that's great evidence that the device is working for you.

Pro tip: Start your renewal process 2-3 months before your current approval expires. This buffer time prevents any gaps in coverage that could leave you paying full price for sensors while waiting for paperwork to process.

Are children or seniors evaluated differently for coverage?

Yes, age does matter when it comes to CGM coverage, but not always in the ways you might expect.

For children, some CGM devices have minimum age requirements. The good news is that pediatric patients often have an easier path to approval because CGMs provide such valuable peace of mind for parents. Being able to monitor your child's glucose levels remotely - especially overnight - is something insurance companies recognize as medically important.

Seniors on Medicare follow the same five-point criteria we mentioned earlier, regardless of age. However, there's one additional consideration: Medicare requires that either the patient or their caregiver can be properly trained on CGM use. If you're caring for an elderly parent with diabetes, you can receive the training and help them manage their CGM.

People with visual impairments may qualify for specialized CGM devices with voice features or other accessibility accommodations. These devices often have streamlined approval processes since they address specific medical needs.

Where can my care team find the latest insurance updates?

Insurance policies change more often than most people realize, which can be frustrating when you're trying to plan your diabetes care. Your healthcare team has several reliable sources for staying current on coverage changes.

Insurance company websites maintain detailed medical policy documents that spell out CGM coverage criteria. These documents can be dense and technical, but they're the official source for what's covered and what's not.

The CGM Insurance Look-Up Tool provides regularly updated coverage information organized by insurance company and state. This tool is particularly helpful for checking multiple plans or comparing coverage options.

CGM manufacturers also maintain detailed insurance information and often have dedicated teams to help with prior authorization paperwork. They have a vested interest in helping patients get coverage, so they stay on top of policy changes.

Many healthcare provider offices employ insurance specialists who make it their job to understand coverage policies and help steer the approval process. These folks are worth their weight in gold when you're dealing with complex coverage questions or appeals.

The key is working with a healthcare team that stays proactive about insurance changes rather than reactive. When coverage policies shift, you want to know about it before it affects your supply of sensors.

Conclusion

Getting CGM covered by insurance is more achievable today than ever before. Most major insurance plans now recognize these life-changing devices as essential medical equipment rather than optional gadgets. The landscape has shifted dramatically in favor of people with diabetes, with Medicare expanding its coverage criteria and several Canadian provinces removing age restrictions entirely.

The secret to approval success? It's all about preparation and persistence. Understanding your specific plan's requirements and working closely with your healthcare team to gather the right documentation makes all the difference. Even if you faced a denial in the past, don't give up - coverage policies are constantly evolving, and what wasn't covered last year might be fully approved today.

We've seen countless patients finally get their CGM coverage approved on appeal, often with just one additional piece of documentation or a peer-to-peer review between doctors. The key is knowing that initial denials are common and don't reflect the final outcome.

At ProMed DME, we've made it our mission to take the hassle out of getting your diabetes supplies covered. Our team works directly with most insurance plans to minimize your out-of-pocket expenses, because we believe managing diabetes should be about your health, not your wallet. We have a dedicated nurse on staff who understands the ins and outs of diabetes management and can answer questions about your supplies and coverage.

The best part? We offer free shipping on all orders, so your CGM supplies arrive right at your doorstep without any extra cost or trips to the pharmacy. Whether you're new to CGM therapy or looking for a supplier who truly understands the insurance maze, we're here to make the process as smooth as possible.

Ready to get started or have questions about your coverage? Learn more about our diabetes supply services and find how we can support you on your diabetes management journey. You deserve access to the technology that can transform your daily life - and we're here to help make that happen.

Related Resources & Articles

Stay informed with our informative blog posts.

Discover the ProMed Advantage

& Try Our Products

We offer free shipping and legendary customer service to ensure you receive the

best DME products for your needs.